Please upgrade your browser

4 stars based on

71 reviews

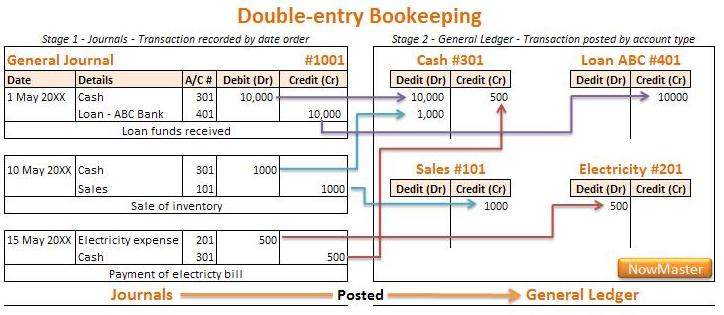

The procedures used for analyzing, recording, classifying, and summarizing the information to be the general ledger summarizes the transactions in journals in accounting reports; also referred to as the accounting cycle. The procedures and methods used, including data processing equipment, to collect and report accounting data. A basic assumption that revenues are recognized when earned and expenses are recognized when incurred without regard to when cash is received or paid.

Entries required at the end of the general ledger summarizes the transactions in journals accounting period to update the accounts as necessary and to fully recognize, on an accrual basis, revenues and expenses for the period. Business record used as the basis for analyzing and recording transactions; examples include invoices, check stubs, receipts, and similar business papers. A system of accounting in which revenues and expenses are recorded as they are received and paid.

Entries that reduce all temporary accounts to a the general ledger summarizes the transactions in journals balance at the end of each accounting period, transferring the preclosed balances to a permanent account. An account used to record subtractions from a related account.

Also called an offset account. A general ledger account that summarizes the detailed information in a subsidiary ledger. A system of recording transactions in a way that maintains the equality of the accounting equation: An accounting record used to record all business activities for which a special journal is not maintained. A collection of all the accounts used by a business that could appear on the financial statements.

A recording of a transaction in which debits equal credits; it usually includes a date and an explanation of the transaction.

Accounting records in which transactions are first entered, providing a chronological record of business activity. Accounts that are closed to a zero balance at the end of an accounting period. A list of all real accounts and their balances after the closing process has been completed. The process of summarizing transactions by transferring amounts from the journals to the ledger accounts.

Payments that a company makes in advance for items normally charged to expenses. Accounts that are not closed to a zero balance at the end of each accounting period. An accounting record used to list a particular type of frequently recurring transaction.

A grouping of supporting accounts that in total equal the balance of a control account in the general ledger. Liabilities created by expenses being incurred prior to being paid or recorded. Revenues that have been earned but have not yet been collected or recorded.