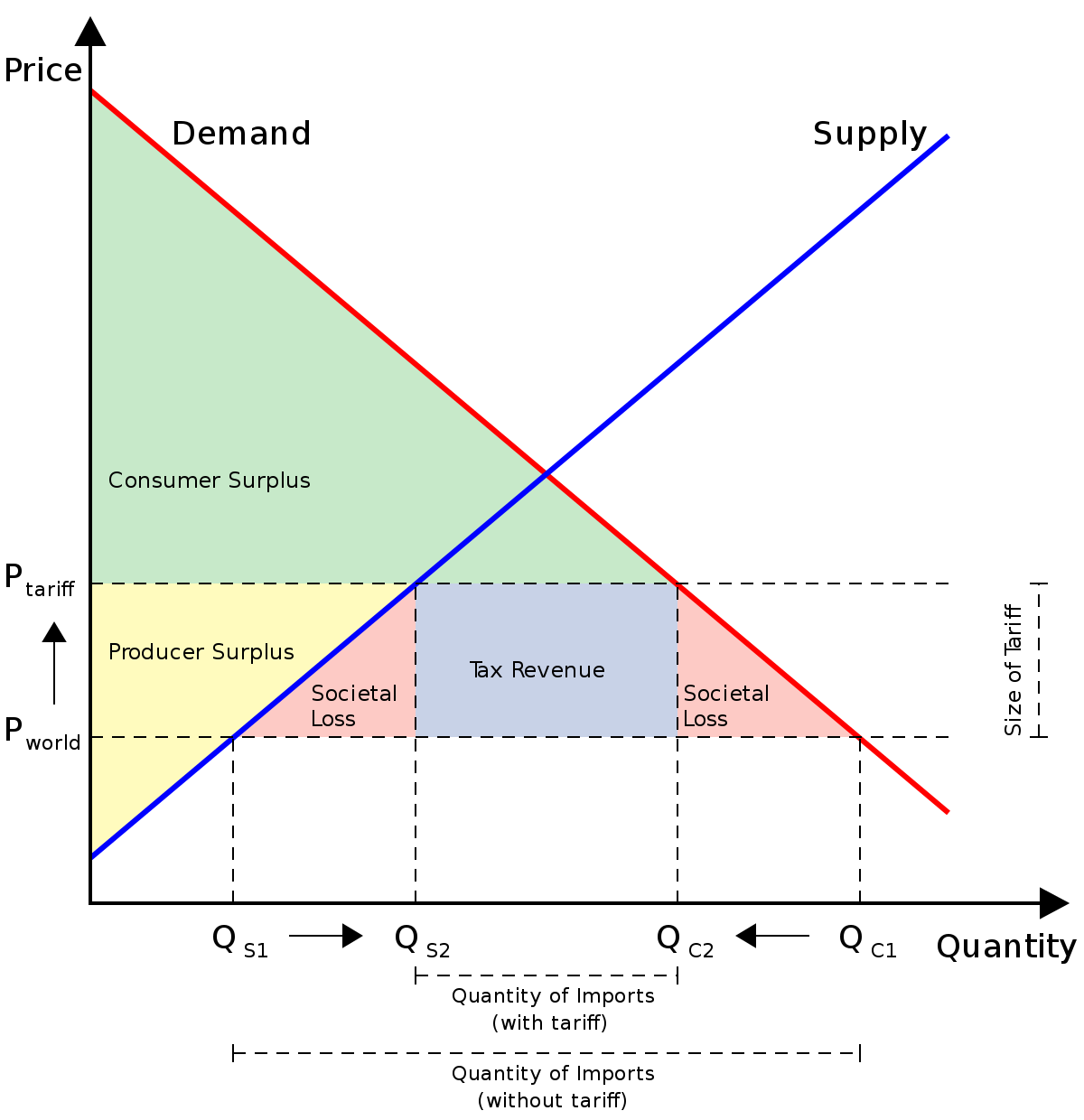

Market transparency liquidity externalities meaning

Scholars have published several papers that evaluate TRACE's impact on liquidity, valuation and other aspects of the U. Abstracts and links to the studies are listed below. Maxwell, Kumar Venkataraman July 20, We study liquidity in U. Despite a temporary increase during the financial crisis, trade execution costs have decreased over time. However, alternative measures, including intraday and overnight dealer capital commitment, dealer participation as principals, turnover, the frequency of block trades, market transparency liquidity externalities meaning interdealer trading, have not returned to pre-crisis levels and in many cases have worsened.

The evidence supports that these outcomes reflect unintended consequences of post-crisis regulations focused on banking. Structured Products, including asset-backed and mortgage-backed securities, comprise one of the fastest growing areas in the financial services industry.

Structured products comprise a significant component of asset allocations in institutional portfolios and the uncertainty associated with their valuation played an important role in the transmission of shocks during the recent financial crisis.

Although these securities are of central importance to financial markets, the secondary market for Structured Products is non-transparent, characterized by market transparency liquidity externalities meaning absence of either public quotations or public reports of transaction prices and quantities. Additionally, Structured Products are unique in their characteristics and customer profiles.

Structured Products can be extremely complex financial instruments with multiple tranches and different payout and risk structures. These products are typically issued by investment banks or their affiliates, and many of the products are market transparency liquidity externalities meaning to retail investors and private bank clients.

The goal of this paper is to provide a first systematic look at the inner working of the secondary market in Structured Products and to the extent possible compare the Structured Products to the corporate bond market to provide implications for market participants when post-trade price reporting is introduced in structured credit products.

We analyze liquidity effects in the US fixed-income securitized product market using a unique data-set compiled by the Financial Industry Regulatory Authority FINRAcontaining all market transparency liquidity externalities meaning between May 16, and February 29, We employ a wide range of liquidity proxies proposed in the academic literature that rely on various information sets.

Our results show that the average market transparency liquidity externalities meaning cost of a round-trip trade is around 66 basis points in the securitized product market and that liquidity is quite diverse in the different market segments.

In particular, we find that securities that are mainly institutionally traded, issued by a federal authority, or with low credit risk, tend to be more liquid. In addition, we discuss the relation between the measurement of liquidity and the disclosure of information, and provide evidence that transaction cost measures computed at a more aggregate level may still be reasonable proxies for liquidity.

This finding is important for all market participants, but particularly for regulators, who need to decide on the level of detail of the transaction data to be disseminated to the market. We show that TBA access translates into enhanced market transparency liquidity externalities meaning with bid-ask spreads of less than 0.

We exploit this unique trade-specific variation in liquidity to generate new estimates of liquidity impacts on prices. This paper examines the liquidity of corporate bonds and its asset-pricing implications using a novel measure of illiquidity based on the magnitude of transitory price movements. Using transaction-level data for a broad cross-section of corporate bonds from throughwe find the illiquidity in corporate bonds to be significant, substantially greater than what can be explained by bid-ask bounce, and closely linked to liquidity-related bond characteristics.

More importantly, we find a strong market transparency liquidity externalities meaning in the time variation of bond illiquidity, which rises sharply during market crises and reaches an all-time high during the recent sub-prime mortgage crisis. Examining its relation with bond pricing, we find that our measure of illiquidity explains the cross-sectional variation in average bond yield spreads with large economic significance.

We study the dispersion of month-end valuations placed on identical corporate bonds by different mutual funds. Our dispersion measures offer insights into corporate bond valuation problems at the individual security level. Results show that pricing dispersion is related to bond-specific characteristics typically associated with market liquidity and market-wide volatility. We also find that the volatile marking patterns of some funds are associated with return smoothing behavior.

However, return smoothing behavior is not prevalent across our sample of bond mutual funds. In this paper, we model price dispersion effects in over-the-counter OTC markets to show that in the presence of inventory risk for dealers and search costs for investors, traded prices may deviate from the expected market valuation of an asset.

We interpret this deviation as a liquidity effect and develop a new liquidity measure quantifying the price dispersion in the context of the US corporate bond market. This market offers a unique opportunity to market transparency liquidity externalities meaning liquidity effects since, from October onwards, all OTC transactions in this market have to be reported to a common database known as the Trade Reporting and Compliance Engine TRACE.

Furthermore, market-wide average price quotes are available from Markit Group Limited, a financial information provider. Thus, it is possible, for the first time, to directly observe deviations between transaction prices and the expected market valuation of securities. We quantify and analyze our new liquidity measure for this market and find significant price dispersion effects that cannot be simply captured by bid-ask spreads.

We show that our new measure is indeed related to liquidity by regressing it on commonly-used liquidity proxies and find a market transparency liquidity externalities meaning relation between our proposed liquidity measure and bond characteristics, as well as trading activity variables. Market transparency liquidity externalities meaning, we evaluate the reliability of end-of-day marks that traders use to value their positions.

Our evidence suggests that the price deviations are significantly larger and more volatile than previously assumed. Overall, the results presented here improve our understanding of the drivers of liquidity and are important for many applications in OTC markets, in general. Beginning on that date, bond dealers were required to report all trades in publicly-issued corporate bonds to the National Association of Security Dealers, which in turn made transaction data available to the public.

In this paper, we assess the impact of the increase in transparency on the corporate bond market. Investors have benefited from the increased transparency, through substantial reductions in the bid-ask spreads that they pay to bond dealers to complete trades. Conversely, bond dealers have experienced reductions in employment and compensation, and dealers' trading activities have moved toward alternate securities, including syndicated bank loans and credit default swaps.

Market transparency liquidity externalities meaning primary complaint against TRACE is that trading is more difficult as dealers are reluctant to carry inventory and no longer share the results of their research. In essence, the cost of trading corporate bonds decreased, but so did the market transparency liquidity externalities meaning and quantity of the services formerly provided by bond dealers.

The debate regarding optimal transparency of the corporate bond markets continues, and the question of what degree of transparency in security markets is desirable will remain the subject of study and debate for the foreseeable future. We develop a simple model of the effect of transaction market transparency liquidity externalities meaning on trade execution costs and test it using a sample of institutional trades market transparency liquidity externalities meaning corporate bonds, before and after the initiation of public transaction reporting through the TRACE system.

The key results are robust to allowances for changes in variables, such as interest rate volatility and trading activity, which might also affect execution costs. We also document decreased market shares for large dealers and a smaller cost advantage to large dealers post-TRACE, suggesting that the corporate bond market has become more competitive after TRACE implementation. These results reinforce that market design can have first-order effects, even for sophisticated institutional customers.

This article reports the results of an experiment designed to assess the impact of last-sale trade reporting on the liquidity of BBB corporate bonds. Overall, adding transparency has either a neutral or a positive effect on liquidity. Increased transparency is not associated with greater trading volume. Except for very large trades, spreads on newly transparent bonds decline relative to bonds that experience no transparency change.

However, we find no effect on spreads for very infrequently traded bonds. The observed decrease in transactions costs is consistent with investors' ability to negotiate better terms of trade once they have market transparency liquidity externalities meaning to broader bond-pricing data.

Using TRACE data—a complete record of all US OTC secondary trades in corporate bonds—we estimate average transaction cost as a function of trade size for each bond that traded more than nine times in We find that transaction costs are higher than in equities and decrease significantly with trade size.

Highly rated bonds, recently issued bonds, and bonds market transparency liquidity externalities meaning will soon mature have lower transaction costs than do other bonds. Costs are lower for bonds with publicly disseminated trade prices, and they drop when the TRACE system starts to publicly disseminate their prices.

The results suggest that public traders would significantly benefit if bond prices were made more transparent. Maxwell, Kumar Venkataraman July 20, Abstract: August 31, Abstract: Liquidity and Value in the Deep vs. August 3, Abstract: